James Macintosh

Nov. 16, 2019

With worries about trade and growth receding, what now?

Investors have short memories, and right now they are busy forgetting everything that supported the market over the summer.

Just a few short months ago, there was a twin argument for why U.S. equities were so high: First, the S&P 500’s defensive stocks provided ballast. Second, there is no alternative to stocks with bond yields so low (an argument so popular it has its own acronym, TINA). Those two factors kept markets near record highs, never mind the escalating trade war and the dire outlook for global growth over the summer.

So, with worries about trade and growth receding, what now? Logically we could expect a reversal: a move back out of defensive and into cyclicals, with rising yields making bonds more attractive than stocks (there is an alternative: TIAA?).

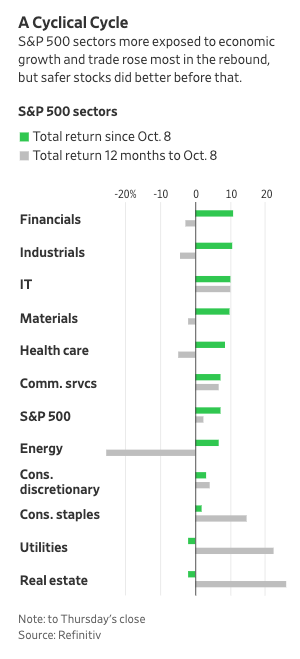

There has indeed been a big move back into cyclical stocks such as industrials and out of defensives such as utilities, as well as a rise in bond yields. Yet somehow the market has been ripping higher, ignoring the previous narrative. Back then, a poor outlook meant lower bond yields, supporting the stock market. Now a better outlook means higher yields, but still supports the stock market. Who needs logic? Just buy.

The S&P was up 8% in the 28 trading days from the start of the rally in October to Thursday’s close, a powerful move that in the past has typically been part of a V-shaped recovery. This time, however, it wasn’t merely a rebound; in the previous 28 trading days the market was only slightly down.

This is an unusual combination. In the past five years, the only moves this big in such a short period have been the upward part of a V-recovery. The next closest was amid the enthusiasm of January 2018; the volatility crash followed within days.

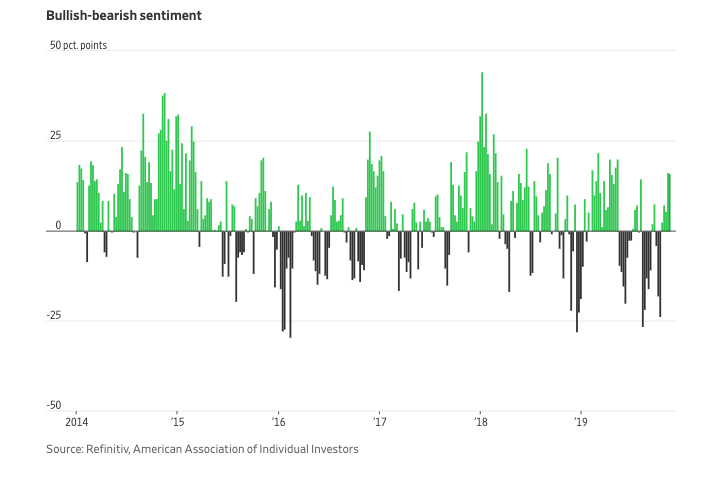

Luckily the mood of the market is quite different today. Back then, investors were wildly overoptimistic on multiple measures, setting them up to fail. Sentiment now is only just recovering from a fairly grim outlook, although it is recovering fast.

For the medium term, the question is whether the reversal of the summer logic will hold back the market. One story is that the market is getting the best of both worlds: fundamental concerns about the economy have eased, yet bond yields remain much lower than they were, helped by the Federal Reserve’s dovish turn. As sentiment toward trade and the economy has improved, those holding cash have decided to put it into stocks, rather than accepting the still-low yield on bonds, helping the entire market.

On this argument, stocks can keep going so long as yields stay below the 2.1% or so that the 10-year offered when the market peaked in July. That leaves room for some further small gains. Beyond that requires a better economy, not just the welcome removal of the threat that it might get even worse.

There is more room for rotation within the market, even if yields keep rising. Relative to defensives, nonfinancial cyclical stocks peaked in April. If cyclicals are going to recover to that level, then the rotation is only half way through.

Ditch the summer logic—perhaps we were all wrong—and the bullish long-run story would be that the market is resuming its trend since the 2009 low. With gains of 13.6% a year for the S&P for the past decade, including dividends, that would be lovely. Could it happen? Something akin to the TINA argument has been used for many years by bulls to recommend stocks, on the basis that no matter how expensive they may appear compared with history, they are still a bargain compared with bonds. Accept this approach, and it is notable that the gap between the real yield on 10-year Treasury inflation-protected securities and the expected earnings yield, the inverse of the forward price/earnings ratio, is the same as it was a decade ago. Stocks are still cheap compared with bonds.

I don’t accept that this implies another decade of double-digit gains from stocks. To duplicate the bull run in stocks would mean valuations repeating their leap since 2009, taking them to the insane levels reached in the dot-com bubble. Profit margins would need to rise even further from what are already elevated levels.

My best case is that the economy muddles through, trade tensions dissipate and earnings turn out to be sustainable, despite leverage and accounting tricks. If it all works out, a return above inflation of slightly under 5% a year including dividends—a bit less than the forward earnings yield—would be a solid long-run return, and appealing compared with about zero after inflation on 10-year Treasurys. When valuations were this high in 2004 and 1997, the next decade delivered after-inflation gains of 4.5% both times, despite enormous market crashes along the way.

But even that is pretty optimistic. It is easy to imagine a future with trade wars spreading from China to Europe, profit margins squeezed by wage rises in a tight labor market and far-higher taxes, all at a time when the world needs to spend heavily to reduce carbon emissions. Valuations could easily fall back toward the lower levels that were the norm in the past, too.

Investors might be willing to switch narrative and keep up the rapid gains for a while longer. But the inexorable logic of a late-stage bull market means future returns will be lower than past gains, even if a recession can be avoided for now.

Write to James Mackintosh at James.Mackintosh@wsj.com

Copyright 2019 Dow Jones & Company, Inc. All Rights Reserved.